In Australia, the common way to generate money is by purchasing an investment property but investors should also be aware that doing so has its own risks and difficulties. That's why if you’re a beginner thinking about purchasing an investment property there are a few things you should know.

To assist you in starting your investment property purchase, we will cover the important points that will guide you with your investment journey.

What is Investment Property?

The act of purchasing a property, typically a commercial or residential one, with the purpose of making money from it is known to as an investment property purchase. Renting it out, selling it to gain money, or doing both are all acceptable options when investing. And those who purchase real estate for investment purposes are called Investors. For the following reasons, the majority of Australians prefer to invest in property:

Generate passive income. This is possibly the most common reason for purchasing a property because you can make money without working hard if you own an asset that generates rental revenue!

Hedge against inflation. As the cost of living rises over time, asset prices typically increase as well. You may guard against price increases and preserve your spending power over time by owning an investment property.

Make a long-term investment. Compared to many other types of investments, like shares and bonds, property investment is frequently far more stable. So f or those looking to invest for the long term, it is the greatest choice as a result.

What are the Tax Benefits of Investment Property?

Although buying an investment property may come with risks it also has significant tax advantages that you won't get from making other types of investments.

Negative Gearing. One of the tax benefits of investment property is that you may be able to claim any money you lose in your investment property from the taxes you've paid through your employment or other investments.

Withdrawals from an equity loan are tax-free. This means that if the value of your property increases and you don't want to sell it, you can acquire a loan from the bank to access a portion of the increase. In short, when you withdraw from your equity loan, you won’t need to pay any taxes.

Depreciation. The reason you can gain tax benefits from depreciation is that when the value of your property lowers, you can claim the lower value and use the money that flows into your pocket in that financial year.

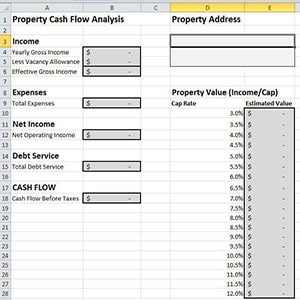

The Cashflow Management

When it comes to investment property purchase, cashflow is one of the most important considerations. Simply put, cashflow is the difference between the rental income you receive and the expenses associated with owning and maintaining the property.

Ideally, you want your investment property to generate enough positive cashflow so that it covers all of your expenses and leaves you with a little extra to pocket each month. Positive cashflow is what allows you to build wealth through real estate investing, while negative cashflow is where your expenses and financing costs exceed the income and you lose money each month.

There are a number of factors that can impact the cashflow of an investment property, such as the location, type of property, and rental rates. As an investor, it's important to do your homework and calculate the estimated cashflow of a property before making an offer. Here’s how you can calculate cash flow:

Determine the gross income from the property.

Deduct all property expenses from the gross income.

Subtract debt service relating to the property.

Use the difference for your cashflow.

The gross income of the property is the total income from any sources before any mortgage payments or expenses are made. Each property will have a different type of expense, therefore, you should determine every expense because calculating it specifically will give you an idea of the cashflow property.

Expenses can include the following:

Property maintenance

Property management

Property taxes

Property insurance

Utility Expense

Business Licenses

What are the Associated Costs?

You must be informed of all connected charges when it comes to investment property in order to determine your financial capacity. To help you, we created a list of all potential connected expenses for you.

Associated Costs when buying an investment property:

Mortgage registration fee. This kind of fee depends on the state you lived in, it will be charged when you registered for a home loan.

Home loans fees. Some lenders will charge a fee for you to apply for a loan, so try to avoid this fee.

Lender’s mortgage insurance. If your house loan is worth more than 80% of the purchase price, your lender will normally ask you to pay the lender's mortgage insurance (LMI). Lenders are protected by this insurance if you skip on your payments. The amount you will pay will depend on your loan, type of property, and lender.

Conveyancing/legal. You will be responsible for paying the costs of conveyancing since he will be the one to prepare the important documents.

Buyer’s agent. They are the ones who help you through your process of finding and acquiring a property.

Stamp duty by the state. This is a tax charged by the state and territory governments on your home value.

Associated Cost when owning an investment property:

Maintenance and repairs. As a landlord, you will responsible for the maintenance and repairs of the property.

Property Management. This is applicable if you want an agent to act on your behalf to find a tenant, they will receive their commission once they sign a new tenant for your property.

Strata/body corporates fees. This applies if you own a property in the form of shared land or title. (i.e. apartment or townhouse)

Insurance. Your property is your valuable asset, so it’s important for you to apply for insurance before you settle.

Utilities. The fees for utilities depend on your agreement, you may be the one to pay for the utilities or your tenant.

Council rates. The landlord or property owner is the one who pays the council rates.

The Current APRA Lending Restrictions

The Australian Prudential Regulation Authority (APRA) increases the minimum interest rate buffer that banks are expended to apply when evaluating the serviceability of home loan applications. APRA has informed lenders that it expects them to assess new borrowers' ability to meet their loan repayments at an interest rate of at least 3.0 percentage points higher than the loan product rate. Because of the increase of the interest rate buffer, new borrowers will likely be affected by this increase. (source: APRA)

Conclusion

If you want to start your investment property, make sure that you choose the right type of property that bests suits your needs and objectives. Moreover, you should understand all the set of risks involved before you commit to anything. Remember that no investment is without risk - but by carefully considering all of the key points in this guide, you can be on your way to success in investment property.